What is the average cost of health insurance in the UK in 2026?

Our updated private health insurance pricing research shows how age, location and policy choices shape your premium.

Andrew has over 20 years of experience in the insurance industry, having worked for household names such as the RAC and Lloyds TSB prior to starting his own brokerage in 2010. An FCA-authorised financial adviser who is a subject matter expert in protection insurance and private medical insurance, Andrew continues to provide clients with a level of service and knowledge that is close to unparalleled.

Full BioHow much is private health insurance in the UK per month?

The average cost of private health insurance in the UK in 2026 is £82.53 per month for an adult, £158.44 for a couple and £180.64 for a family of four, according to myTribe's analysis of 11,770 quotes.

The quotes were gathered in March 2026 from seven of the UK's leading insurers, for people aged 20 to 70 in 21 towns and cities across England, Wales, Scotland and Northern Ireland. We believe this is the most comprehensive analysis of UK health insurance pricing currently available.

Source: myTribe 2026 Private Medical Insurance Research (11,770 quotes, seven insurers, March 2026).

Full age-band tables for couples and families sit in our couples pricing guide and family pricing guide, and several insurers offer multi-policy discounts. A joint couple's policy costs about 4% less than two separate single policies, and adding a third child costs less than £9 a month at every parent age. You can compare quotes from the UK's leading insurers with advice from a vetted broker through myTribe.

Why are more people buying private health insurance?

More people are buying private health insurance because NHS waiting lists remain high. The latest NHS England figures, for April 2026, show 7.22 million incomplete treatment pathways still waiting. Lord Darzi's independent investigation in September 2024 found problems across most of the health system, and progress since has been slow.

The pressure is not limited to planned surgery. The National Health Service is also stretched on cancer care, mental health, dentistry and GP services, pushing more people to look for faster private treatment.

That is showing up in the data. According to the Association of British Insurers, private medical insurance membership reached a record 6.5 million UK lives in 2024, up 4% year on year, with claims paid rising 13% to £4 billion, almost £11 million a day. Workplace schemes hit their second consecutive record across more than 30 years of ABI figures.

Why you can trust myTribe Insurance Experts

- 11,700 private health insurance prices gathered first-hand for our annual pricing study, covering all four UK nations and 21 towns and cities

- Seven leading UK health insurers analysed side by side on a like-for-like basis, so the comparison is fair

- Independent and impartial, with no commercial relationships with any insurer, so what we publish is not shaped by who pays us

- Over a decade spent researching and explaining UK private health insurance

- Regularly cited by the national press, including BBC News, The Times, The Guardian and the Financial Times

Your age and cover level are two of the biggest influences on what you pay for private health insurance, because the risk of medical conditions such as cancer, stroke and heart disease rises as we get older, and treating them privately cam be expensive. A 20-year-old pays on average £28.54 a month for basic private health insurance cover, while a 70-year-old pays more than five times that at £151.04.

The table below shows the average monthly cost in 2026 for a basic plan and for comprehensive health insurance cover, which adds outpatient cover and complementary therapies.

How have private health insurance prices changed since 2025?

New private health insurance prices have risen by around 1% since myTribe's 2025 research, though some insurers moved more than others. The biggest rise was for 70-year-olds on basic cover, up about 4.8%. Comprehensive cover was more mixed: younger adults paid around 3% more, while cover for 60 and 70-year-olds came down by 1% to 2%.

Health insurance renewal premiums usually rise faster than new-policy prices, owing to changes in your discount and the impact of claims, so it can be worth reviewing your cover and insurer at least every two years.

What our health insurance expert says:

"New health insurance policies usually start with a 65% to 70% no-claims discount, which is reflected in our research. At renewal, your discount often changes based on claims activity, with some insurers doing that more gradually than others. When getting health insurance, the rules around claims and premiums play the biggest role in long-term affordability."

Chris Steele, Founder and Insurance Expert (Cert CII)

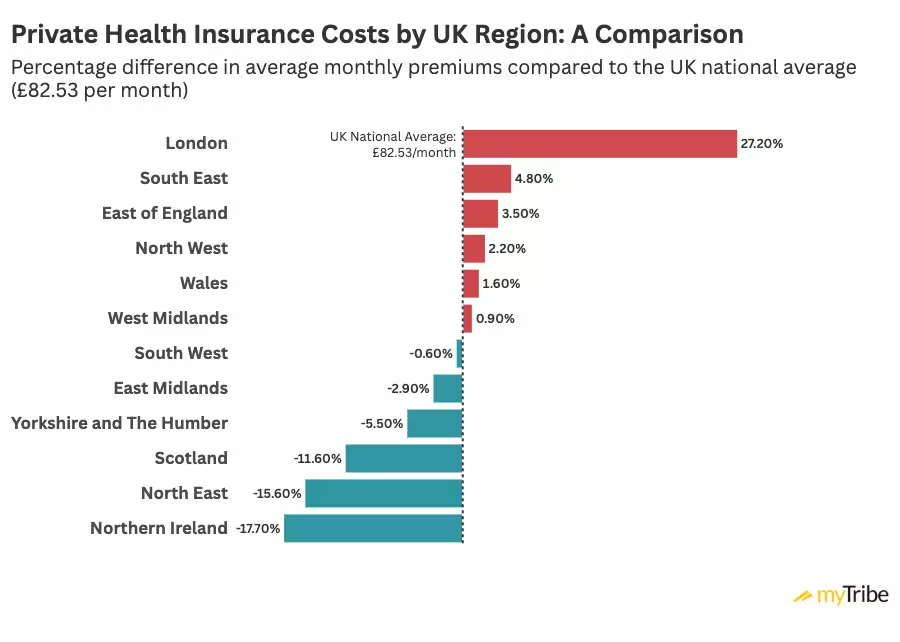

Most private health insurers price by postcode, so where you live often directly impacts what you pay. Private health insurance costs vary across the country as hospital and consultant fees differ from region to region. London is the most expensive region at 27.2% above the national average, while Northern Ireland is the cheapest at 17.7% below.

We grouped our 21 postcodes into the UK's 12 regions. The figures combine basic and comprehensive cover, so you can see the regional pattern rather than the effect of cover level.

A 50-year-old in a London postcode pays roughly £444 a year more than the same person in Belfast, because private hospital costs and consultant fees are concentrated in the capital and claims tend to be more frequent. One exception: Freedom does not price by postcode, so your region has no bearing on a Freedom quote.

No single health insurer is the cheapest for everyone. The best price depends on your age, the cover level you want and where you live, though the gap between the cheapest and most expensive insurer can run to hundreds of pounds a year.

Our 2026 research compares seven health insurers: Aviva, AXA Health, Bupa, Freedom, The Exeter, Vitality and WPA. All prices below are monthly premiums for a single policy with a £250 excess (£200 for Aviva), on moratorium underwriting. Plans are not identical: Freedom and WPA, for example, do not operate a guided consultant list, so their default prices give access to a wider pool of specialists. Always compare what is included, not just the headline premium.

Comprehensive health insurance adds outpatient cover for specialist consultations, diagnostic tests and scans on top of inpatient treatment, and is the most common type of private health insurance in the UK.

Bupa is the most consistently competitive health insurer for comprehensive cover in our 2026 research, with the lowest premium at ages 30, 40 and 60 and a place in the cheapest three at every age. AXA Health also appears in the cheapest three at every age, with the lowest premium for 50-year-olds at £76.12 a month. Vitality is the cheapest at 70, at £162.91 a month.

On basic cover, the cheapest health insurer also varies by age. Bupa and The Exeter each sit in the cheapest three at five of the six ages we tested, WPA offers the lowest basic premiums for younger customers (from £16.03 a month at 20), and Vitality is cheapest at 60 and 70.

Shopping around matters most in later life. On basic cover the gap between the cheapest and most expensive insurer is under £20 a month at 30 (about £236 a year), but widens to more than £100 a month at 70, or £1,214 a year. In your 30s, cover features and service matter more than price.

What our health insurance expert says:

"Comparing insurers on price alone is never perfect. The plans vary, and what looks cheaper on paper might not cover the treatment you actually need. It is worth checking whether a policy uses a guided consultant list, what outpatient treatment cover is included, and how the insurer handles claims at renewal. A broker can usually compare these details faster than you can alone."

Chris Steele, Founder and Insurance Expert (Cert CII)

The cheapest type of private medical insurance is a treatment-only or basic plan, which gives you core cover without optional extras. The average basic policy costs £66.55 a month in 2026, against £98.53 a month for comprehensive cover.

What does core cover include?

Most basic plans cover:

- Inpatient and day-patient treatment in a private hospital

- Outpatient surgery

- Cancer treatment and care

- Some complex scans, such as MRI, CT and PET

- Virtual GP services

- Physiotherapy, in some cases

Basic plans offer a range of benefits but will not include all the benefits a comprehensive policy would. With a cheaper plan you usually need a diagnosis before you can claim private treatment, so you either go through the NHS first or self-pay for tests and consultations. The cheapest provider varies by age: WPA at 20 (£16.03), Bupa at 30 (£29.19), The Exeter at 40 (£37.90), AXA Health at 50 (£52.71) and Vitality at 60 and 70 (£74.26 and £105.28). That spread is why shopping around pays off.

Several factors shape what you pay for private health insurance. Three of the biggest are your age, your cover level and where you live. The others are set out below.

The cost of private medical treatment

Premiums track the cost of private medical treatment, and those costs tend to rise. According to Statista, the price of health-related products and services in the UK was 42.4% higher in 2026 than in 2015. Advances in treatment explain part of this, but private hospitals also face rising running costs, which feed through to premiums.

Your current health

Some health insurers reward good health at the point you take out cover. Vitality offers a 15% discount through its Mori+ underwriting if you have had no symptoms, advice or treatment in the past three years. Aviva gives 15% if you are a healthy weight, have not recently smoked and do not have diabetes. Bupa offers 10% if you do not smoke, have not been treated for diabetes or pre-diabetes in the past two years, and have a BMI between 18.5 and 24.9.

Your claims history

A new policy usually starts with a no-claims discount of around 65% to 70%. Health insurance works in reverse to car insurance: you begin near the top, and claiming can move you down the discount levels, lifting your premium over time. An alternative, community rating, sets increases by the claims experience of all members rather than your own, but every major insurer has now withdrawn community-rated cover for new customers.

Overall claims volumes

Premiums also reflect how much the insurance industry pays out in total, not just what you claim yourself. When claims across the whole market rise, most insurers raise prices for everyone at renewal. NHS pressure feeds this directly: the longer the waits, the more members use their private medical insurance rather than hold off, which pushes total claims, and prices, up.

Whether you use nicotine

If you smoke, vape or use nicotine products, your premiums may be higher, though not always. Nicotine replacement is generally considered safer than smoking, but long-term evidence is limited, so unless you stop altogether you may pay a little more.

Two policy choices also move your premium: a higher excess and a guided consultant list. Both can cut your costs, and we cover them next.

The biggest way to cut your premium is usually a guided consultant list, where your health insurer helps choose who treats you and where, in exchange for a lower premium. The alternative, freedom to choose your own consultant on a standard hospital list, costs more. Our research shows the guided option cuts premiums by around 16% on average, though it reduces your choice of consultant and hospital. You can see how guided and standard cover compare in our guide to guided consultants.

A higher policy excess is the next lever: as a rule, the higher your excess, the lower your monthly premium. Moving from a £0 to a £250 excess saves around 14% on average, and a £500 excess around 23%, though you pay more towards each claim. Our guide to how excess affects your premium has the full age-by-age figures.

Other ways to bring the cost down include limiting or removing outpatient cover, dropping optional extras, and adding a six-week NHS wait, where you only claim privately if the NHS cannot treat you within six weeks. For more options, see our guide to saving money on health insurance.

Is health insurance more expensive for smokers?

People who smoke, or who have used nicotine products such as vapes, patches or gum in the past couple of years, usually pay a little more for medical insurance. The increase is often modest, especially compared with life insurance. The bigger effect tends to come later: smoking-related illnesses that lead to claims can push up your renewal price over time. Our guide to health insurance for smokers covers this in more detail.

Does health insurance cost more with pre-existing medical conditions?

Private health insurance is not usually loaded for pre-existing medical conditions. Instead, health insurers exclude those conditions through your underwriting terms. You might pay a little more than someone in perfect health, simply because you would not qualify for the 10% to 15% good-health discounts some insurers offer.

If you have pre-existing medical conditions or a complex medical history, a broker can help you choose the right type of medical underwriting and point you towards the insurers most likely to suit your circumstances.

How we assessed the average cost of health insurance

Private health insurance can be configured in many ways, so we standardised the quotes as far as possible to give meaningful guide prices.

Our data sample

We priced cover for one adult, couples and families, with the main applicant aged 20, 30, 40, 50, 60 or 70. For each age we gathered quotes from 21 UK towns and cities: Belfast, Birmingham, Bournemouth, Cambridge, Cardiff, Colchester, Coventry, Edinburgh, Exeter, Leeds, Leicester, London (West), London (South East), Manchester, Newcastle upon Tyne, Nottingham, Oxford, Reading, Sunderland, Wirral and York. We took quotes from seven of the UK's best private health insurance providers, with and without outpatient cover.

How we configured each quote

Working with external brokers, we set a consistent basic and comprehensive specification:

- Basic: no added outpatient or therapies cover.

- Comprehensive: outpatient cover capped at £1,000 a year, plus therapies cover.

- Excess: £250, or as close as possible (£200 for Aviva).

- Mental health cover: excluded, except for Bupa, which includes it as standard.

- Hospital list: each insurer's standard hospital list.

- Dental, optical and travel cover: excluded.

- Underwriting: moratorium basis.

- Consultant list: guided, where the insurer offers one (WPA and Freedom do not).

Quote data was collected in March 2026. Prices come from the Aviva, AXA Health, Bupa, Freedom, The Exeter, Vitality and WPA websites, with product details last verified in May 2026.

This is general information, not personal advice. Consider speaking to a qualified broker before you decide. Our broker partners compare policies from a panel of leading UK insurers, though not every insurer may be available. To get a comparison quote for health insurance based on your situation please click here.

What our readers say

We're rated Excellent on Google from 160+ reviews. Reviews relate to the service provided by both myTribe and our broker partners.

"The information was very helpful and informative. They put me in touch with an extremely helpful broker. I am now moving to a different provider, on a better policy, at a much reduced premium."

"Absolutely straightforward experience. The lesson? NEVER accept a renewal quote without shopping around!"

"Saved time and gave me a lot of insight. I could not have done that on my own."

Disclaimer: This is general information, not personal advice. Speak to a qualified broker before making a decision. Our broker partners compare policies from a panel of leading UK health insurers, but not all insurers may be available.

Frequently Asked Questions

Does private health insurance include cover for cancer care?

Private health insurance usually includes cancer cover, though the level of cancer care varies between policies and cover levels, so check the wording. Most comprehensive policies cover the active treatment of a new cancer, such as surgery, chemotherapy and radiotherapy, while cover for longer-term or ongoing cancer care varies, with some health insurers paying in full and others setting limits.

Will I pay more buying health insurance cover through a broker?

No, buying through a broker does not usually cost more. Brokers normally have access to the same prices as buying direct from a health insurer. The added benefit is tailored advice on the pros and cons of each plan, so you can compare what is actually covered rather than just the headline price.

Where is the cheapest place to buy private health insurance cover?

Belfast is the cheapest UK city for private health insurance, at an average of £67.91 a month for one adult, around 17.7% below the UK average. Newcastle, Sunderland and Edinburgh are also at least 11% below average.

What is the most affordable type of health insurance?

The most affordable type of health insurance is a treatment-only plan, which offers core cover, including inpatient and day-patient hospital treatment. Health insurance premiums rise as you add additional cover options to your plan, such as outpatient cover, mental health cover and more

Why do health insurance premiums usually rise at renewal?

Health insurance premiums usually rise at renewal for three reasons: you are a year older, private medical treatment has become more expensive, and your no-claims discount can fall if you have claimed. If your renewal rises sharply, comparing plans can show whether you could switch and pay less without losing cover.

Is it cheaper to pay health insurance monthly or annually?

Paying monthly or annually usually costs the same overall with most health insurers. A few offer a discount of around 5% to 6% for paying annually.

What is a health insurance no-claims discount (NCD)?

A no-claims discount (NCD) is a reduction off your premium, often 65% to 70% at the start, that you keep by not claiming. Unlike car insurance, where you build a discount over time, private medical insurance usually starts you near the top, so claiming can move you down and push premiums up.

Will a larger excess reduce my health insurance premiums?

Choosing a higher private health insurance excess will usually reduce your monthly premium, but it's worth working out how the reduction you'll get, as in some cases, the saving versus the excess increase isn't worth it.

When you get quotes, ask your broker to show you the prices for different excess levels, so you can see how much of a saving you'll get by increasing it.

Is cost the most important factor when buying health insurance?

While the cost of private health insurance is an important consideration, it should be balanced with making sure your policy provides you with the benefits you need and value.

In many cases, the cheapest health insurance policy isn't the best. By paying a bit more for your cover, you may find that you get a private medical insurance plan that's much better suited to your requirements.