How to get the best deal on your health insurance renewal

When your medical insurance renewal arrives, the premium will almost certainly have risen, sometimes a little, occasionally a lot. The good news is that you have more control over the price than most people realise, with five practical levers to pull, although switching providers carries an underwriting catch that is worth understanding before you act. This guide explains how UK health insurance renewals work and how to pay less.

Richard Eagling is the Senior Editor at myTribe, with 25+ years in personal finance journalism and a CII Certificate in Financial Services. Previously at Moneyfacts and NerdWallet UK, his work has featured in The Guardian, BBC and The Telegraph.

Full BioHow can you get a better deal on your health insurance renewal?

There are five main ways to reduce what you pay when your health insurance renews:

- Get health insurance comparison quotes to see whether changing insurer would save you money.

- Contact an experienced health insurance broker for independent market advice.

- Haggle with your existing insurer, ideally armed with competitive quotes from elsewhere.

- Consider adjusting your policy benefits, such as your level of outpatient cover, and removing optional extras you no longer need.

- Look at your voluntary excess and work out whether it makes sense to increase it.

Comparing plans and changing health insurer at renewal is often relatively straightforward, but there are pitfalls to be aware of, and the biggest is the risk of new medical exclusions, which we explain later. It is not something we suggest doing without getting expert advice first.

myTribe works with a panel of vetted, experienced brokers. If you would like expert help, please request a comparison quote and we will match you with one that specialises in helping people who already have health insurance.

Who is this health insurance renewal guide for?

This guide is for individuals, couples and families in the UK who have a personal private medical insurance policy, whether bought directly from an insurer or through a broker. If the renewal letter is addressed to you and you pay the premium, this guide is for you.

It is not written for businesses or for employees with company health cover through a group scheme, because those renewals are calculated differently. Group schemes are usually experience rated, meaning the whole scheme's claims feed into the price rather than a personal no claims discount. If that is your situation, our small business health insurance guide will serve you better, and if you are leaving a job and want to keep your cover, see continuing health insurance after leaving your employer.

Almost every health insurance renewal brings an increase, because private medical treatment costs rise each year and you are a year older every time your policy renews. Claims you have made in the past year, rising administration costs, and in some cases your activity levels and health all feed into the price too. So does the claims activity of your existing provider's wider customer base. The Association of British Insurers reports that insurers paid a record £4 billion in private medical insurance claims in 2024, up 13% on the year before, and rising claims across an insurer's whole book feed into everyone's renewal.

How much do health insurance premiums rise each year?

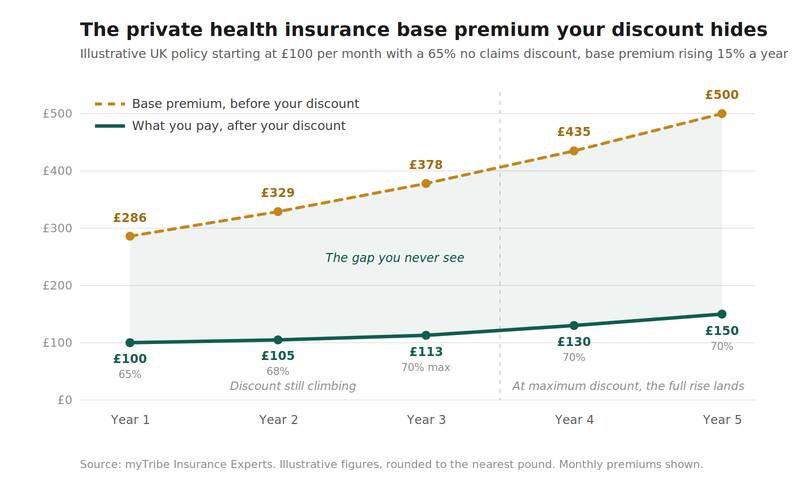

Health insurance base premiums, the cost of a policy before any no claims discount is applied, rise by around 15% a year in the UK. That is what myTribe’s analysis of insurer pricing consistently shows, with medical inflation doing most of the work. Insurer surveys by WTW put UK healthcare cost inflation at 10.6% in 2025 and around 10% for 2026, among the highest in Western Europe, and being a year older at each renewal makes up the rest.

Most policyholders never see that 15%, because their no claims discount masks it. The majority of UK health insurers start new customers with a discount of between 64 and 72%, so the price quoted on day one is already a heavily discounted version of the real cost. While your discount is still climbing, each step up the scale absorbs part of the base premium increase, which keeps your early renewals looking deceptively modest.

Here is how that plays out for a policy costing £100 per month with a typical 65% starting discount.

Two things follow. First, once you reach your insurer's maximum discount, usually within two to three claim-free years, there is nothing left to soften the increase, and the full base premium rise lands on your renewal despite you never having claimed. Second, claiming triggers a double hit, because the base still rises by around 15% while your discount falls at the same time. A drop from 65% to 55% on the policy above would take year two from £105 to £148 per month, a 48% increase, not the 10% the discount change suggests.

You can work out your own policy's underlying cost with our base premium calculator, and we unpack the full mechanics in why health insurance premiums rise every year.

When is my health insurance no claims discount for next year calculated?

Health insurance no claims discounts are calculated in the weeks or months before your renewal date rather than on the day itself, although not all insurers offer one. Most insurers work the discount out between six weeks and three months ahead, so the figure that sets your renewal price is effectively fixed before your renewal arrives.

Exactly how far ahead depends on the insurer, with Bupa calculating yours around six weeks before renewal and AXA Health and Saga looking up to three months ahead. The Exeter instead assesses a fixed window, the last two months of your previous policy year plus the first ten months of the current one. This timing matters because a claim made shortly before renewal often falls outside the window, so it will not reduce your discount until the year after that.

Yes, UK private health insurance policies auto-renew annually with no action needed on your part, so you do not accidentally lose cover. Your insurer has to give you enough time to consider your options, but the responsibility to review whether the plan still meets your needs, and to compare other options, rests with you.

In practice, most UK health insurers issue renewal notices 21 to 30 days before your renewal date, so you will usually see your new price three to four weeks out. The Financial Conduct Authority (FCA), which regulates private medical insurance alongside other financial products, only requires firms to provide your renewal notice in "good time" before the renewal is due, so there is no precise rule, and each insurer takes its own approach.

Your health insurance renewal notice must show your new premium alongside your premium for the past year, presented so the two are easy to compare, together with enough information to check your cover is still appropriate and a statement on whether the contract will renew automatically. These rules were introduced by the FCA in April 2017 for general insurance firms, which includes private medical insurance providers, to improve the treatment of existing customers and encourage people to shop around.

If you have been with the same insurer for four or more consecutive years, the firm issuing the renewal notice must also include this statement: "You have been with us a number of years. You may be able to get the insurance cover you want at a better price if you shop around."

The regulator added that prompt for good reason. Renewal pricing rewards the customers who compare, so a policy that never gets a market review can drift well above the going rate, and failing to review your cover at renewal can quietly become overpaying for it. Insurers also use the renewal notice to flag any changes to your policy terms for the year ahead.

Firms must present all of this clearly, in a way that draws attention to the key information.

Sources: FCA Policy Statement PS16/21, FCA Handbook ICOBS 6.5 Renewals

When should I start comparing health insurance policies before renewal?

Start comparing health insurance options 30 to 60 days before your renewal date. You probably will not start a new policy until your current one ends, but these are complex products, and an early start gives you time to research the insurers, understand their relative strengths and weaknesses and get unbiased advice. It will also save time later, because when your renewal quote arrives you will already have a shortlist and a head start.

Can I move to a new health insurer after my current policy has renewed?

Yes, you can move to a new health insurer for up to 14 days after your policy renews. Every UK health insurance provider gives you a 14 day cooling off period, and it applies to automatic renewals too, so you can cancel and move elsewhere even after your renewal date has passed.

Health insurance can also be cancelled mid term, but switching providers mid term is harder, you will likely have to accept a new provider's medical underwriting terms, and you may need to pay a cancellation fee too.

Review your health insurance every year, and do a full market review at least every other year or whenever you face a large increase. Depending on the size of the rise and when you last reviewed your cover, switching providers may not be something you need, or have time, to do every single year.

The larger renewal premium rises tend to arrive after a few years of holding health insurance, either because you have claimed or, ironically, because you have reached your current provider's maximum no claims discount and it is no longer offsetting base premium rises. We believe that amounts to a form of "loyalty penalty", and it does not feel entirely fair, because it hits hardest the customers who have never claimed. If you have been with your current insurer for some time, there is a good chance a market review could save you money.

When should I haggle with my existing health insurer?

You can haggle with your existing provider at any time between receiving your new price and your renewal date, although you will be in a stronger position if you enter those negotiations armed with competitive quotes from other providers. If you would like a market review, please request a quote through myTribe and we will match you with an independent broker that's experienced in helping people review their policies and negotiate with their current insurer, so you have everything you need to haggle.

When you start your market review, whether researching your options yourself or with help from a broker, there are three vital questions to ask.

1. Will changing health insurance provider introduce new medical exclusions?

It is often possible to "switch" health insurers on similar terms and avoid or minimise new medical exclusions, because some insurers offer switch underwriting that carries across the conditions already covered. This depends on your medical history and is never guaranteed. If you cannot switch on existing terms, you would be re-underwritten, and conditions that developed while on your current policy could then be excluded from your new policy as pre-existing conditions.

2. Are you comparing like-for-like health insurance plans?

All health insurance policies are different, in ways that range from the obvious to the subtle. Knowing your current policy terms, from your benefits and exclusions through to which hospitals and consultants you can access, matters before you choose a new policy. It is easy to assume these products are all the same, but as our health insurance ratings highlight, that could not be further from the truth.

3. How might claims affect future health insurance premiums?

Every UK private medical insurance provider has different rules on how claims affect future premiums, and some are more transparent than others. A new provider that offers better value in year one could cost you more over time if its rules are harsher, so check how each insurer's no claims discount works before you move.

What our readers say

Our insurance information and comparison service is rated Excellent on Google from 170 reviews as of 6th August 2026.

Good support great knowledge caring empathetic and totally understanding

"The information was very helpful and informative. They put me in touch with an extremely helpful broker. I am now moving to a different provider, on a better policy, at a much reduced premium."

"Absolutely straightforward experience. The lesson? NEVER accept a renewal quote without shopping around!"

Disclaimer: This is general information, not personal advice. Speak to a qualified broker before making a decision. Our broker partners compare policies from a panel of leading UK health insurers, but not all insurers may be available.

Frequently Asked Questions

Can I cancel my health insurance contract at any time?

Yes, you can cancel your health insurance contract at any time, though what you get back depends on when you cancel. Within the 14 day cooling off period, at the start of the policy or at renewal, you can cancel and, so long as you have not used the policy, have some or all of your premium refunded. After that, if you pay annually you are usually refunded for the unused part of the year, while if you pay monthly you simply stop future payments, so it is worth checking your own policy terms for any conditions that apply.

Can I change my health insurance cover or who is insured at renewal?

Yes, renewal is the natural point to adjust your health insurance cover, whether that is your excess, your benefits or who is on the policy, and your existing cover usually continues unaffected. Changes that increase your cover, such as adding a benefit or a new family member, may be subject to underwriting for the new element.

Is the health insurance renewal process different for businesses and individuals?

The mechanics of renewing health insurance are similar for both, policies auto-renew and you receive a renewal notice, but business schemes are often priced differently. Larger schemes are usually experience rated, meaning the whole scheme's claims feed into the price rather than a personal policy's no claims discount, and they are typically reviewed with a broker each year.