Why is health insurance so complicated?

Buying something as important as private health insurance (also known as private medical insurance, PMI) should be straightforward. In reality, it often isn’t, and it can feel overly complex. It could even mean you end up with a policy that doesn’t give you the cover you need or want. Here, we look at demystifying specific aspects of private health insurance, so that you can choose a policy that’s right for you.

1-minute read about why health insurance is so complicated

Health insurance is often expensive due to various factors, including the thorough assessment of risk by insurers, the breadth of coverage offered, additional features like mental health treatment, and payment options such as excess and shared responsibility. Age and health status also influence premiums, as do regulatory requirements and the rising cost of healthcare. Overall, the complexity of health insurance, coupled with the need to balance coverage and affordability, contributes to its high cost.

Related guides:

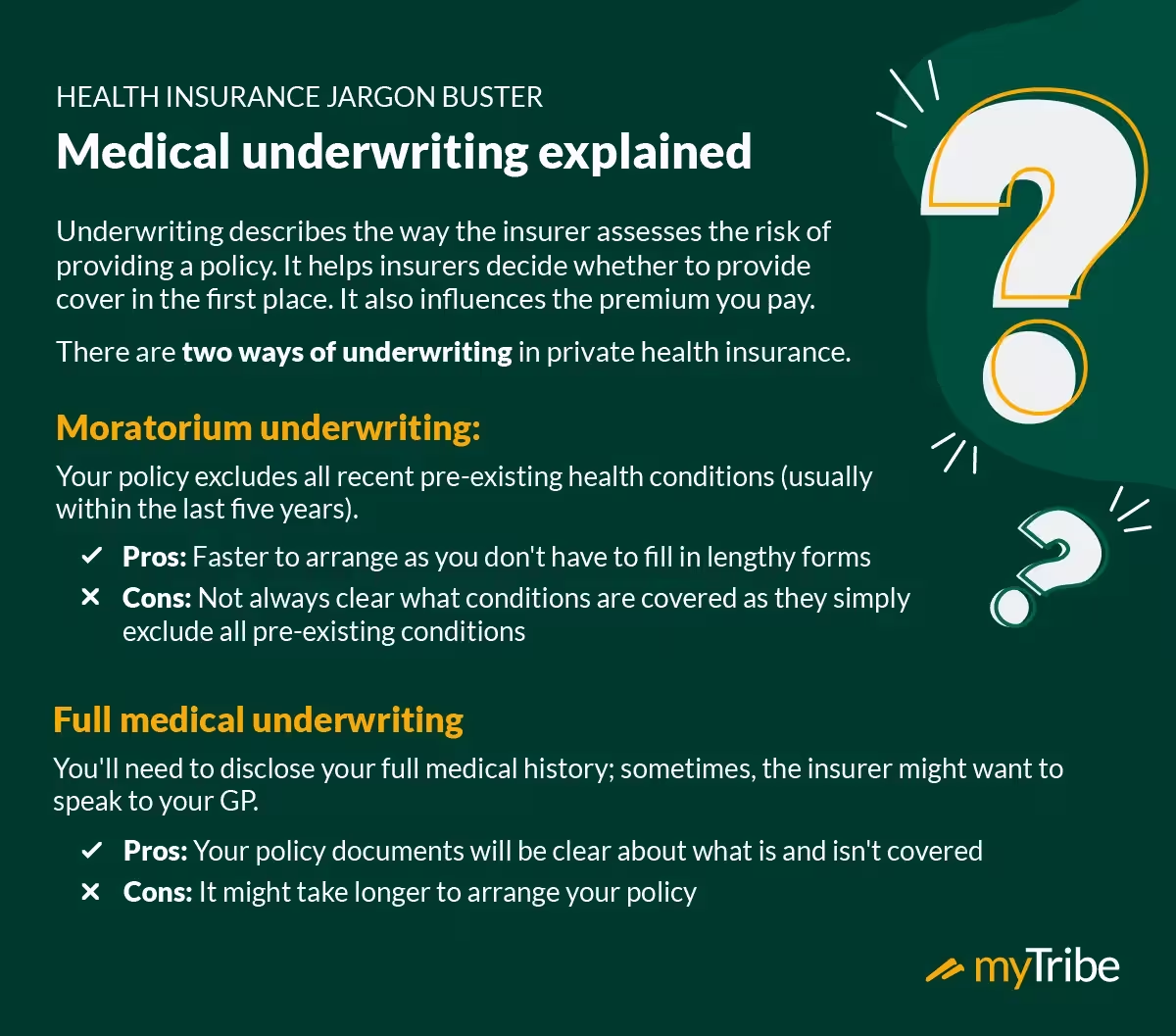

Underwriting is a term that describes the way risk is assessed. All insurance products, including your home and car cover, go through the underwriting process.

The outcome of the process helps insurers to decide whether to provide cover in the first place. It also influences the premium you pay.

In health insurance, new policies can be underwritten in one of two ways:

Moratorium underwriting

Moratorium underwriting is when your policy excludes all recent pre-existing health conditions (usually within the last five years). A pre-existing condition is any illness or condition that you've:

- Had symptoms of

- Been diagnosed with

- Had treatment for

- Sought advice for

However, so long as you are symptom-free for a certain period of time (normally two years) cover for that particular condition may be reinstated.

One of the benefits of choosing a policy with moratorium underwriting is that you won't need to complete lengthy questionnaires about your health when you apply, making moratorium policies much faster to arrange.

The downside is that moratorium policies are not always clear about what conditions are covered as they simply exclude all pre-existing conditions. It means that each time you make a claim, your insurer will ask about your medical history and may need to look at your records. To do this, they will usually speak with your GP. This can also lead to lengthy claims processes as your insurer will need to verify the claim before they agree to cover treatment.

Full medical underwriting

If you choose a policy with full medical underwriting, you'll need to tell your insurer about your medical history. Typically, this means filling out a lengthy health questionnaire, and it could include a medical, depending on the insurer. In some cases, insurers will also need to speak to your GP or other health professional, particularly if there are points they need to clarify.

The benefit of gathering all this information upfront is that your policy documents will be clear about what is and isn't covered, so the claims process should be straightforward. You may even find some pre-existing conditions are covered by your policy even if you've experienced them relatively recently.

The downside with full medical underwriting is that policies usually take longer to arrange. Removing any exclusions (conditions that aren't covered) can be harder, too.

PMI typically only covers acute conditions – these are illnesses that can be successfully treated with medical care. For example, broken bones, appendix surgery, cataracts and hernias.

As a broad rule, health insurance does not cover chronic conditions (conditions that can only be managed and not cured). Chronic conditions include diabetes, high blood pressure (hypertension), and arthritis.

There may be exceptions depending on the stance taken by the insurer. In many cases, private health insurance will cover acute flare-ups of a chronic condition. For example, asthma might be excluded from your policy but if you had an unexpected asthma attack that required hospitalisation, your health insurer may cover this.

Similarly, while cancer can be considered a chronic condition, cancer care is often a key feature of many private health insurance policies. Again, the level of cover you receive will vary according to the insurer, so be sure to check the terms of your policy.

Private health insurance doesn't normally cover cosmetic treatments either. That said, Vitality does cover some of the cost of a handful of 'corrective' treatments, such as ear reshaping (pinnaplasty) and breast reduction surgery (for men and women).

Looking for affordable health insurance?

Request a free comparison quote, and we’ll connect you with the an experienced broker best suited to help.

Compare Quotes

One of the most confusing aspects of health insurance is terminology, as insurers use different names for essentially the same things. Some terms can also be deceptive, so what one insurer calls a comprehensive policy might not be the same as another.

Specific terminology to be aware of includes:

Guided consultant list

Choosing a guided list means your choice of consultant is limited to those your insurance provider has shortlisted. Each one will, of course, be a specialist in the field you need treatment in.

Depending on the insurer, the list of specialists may still be quite long, whereas others may suggest just two or three. Choosing a guided option can also keep premiums down.

Guided consultant lists are known by all sorts of different names, including:

- Expert select

- Guided care

- Guided option

- Consultant select

The alternative to a guided consultant list is a "non-guided" list. This option will mean you can choose your own specialist consultant, but it usually leads to higher premiums.

Before we talk about hospital lists, we should point out that most insurers will also suggest which hospital you should use for your treatment as part of their guided option. So, in most cases, if you go for a guided list, you won't get much choice over where you are treated.

Hospital network

If you opt for non-guided consultant access, most insurers will give you the option to choose a hospital list, covering varying quantities of private hospitals around the UK.

If you don't want to limit your choice of hospital, you can opt for a national or unrestricted hospital list instead, but this will make your policy more expensive.

It's worth bearing in mind that consultant lists may also be tied to your choice of hospital network and vice versa.

Mental health support and treatment

A number of health insurance providers advertise mental health services, but there's often a big difference between what's termed mental health support and mental health treatment.

Support can include services such as wellbeing guidance or access to counselling. In most cases, mental health support is only accessible remotely by phone or video call. Services may also be limited to a handful of sessions which means if you wanted to continue, you'd have to cover your own costs.

Mental health treatment, on the other hand, is usually an optional extra but covers specialist psychiatric care and face-to-face services. For example, inpatient treatment for eating disorders or substance abuse.

Health insurers will consider a wide range of factors to work out your premium. Some of these factors are intrinsic, in other words, it's about the policy itself and how it's made up. For example, the features you choose, options you add and how the policy is underwritten. Your age, job and lifestyle also affect your premium.

- Find out more: The cost of private medical insurance cost in the UK

As well as these essential elements, what you pay for health insurance is also affected by certain pricing methods. These are options given to you by the insurer in order to help you keep costs down, for example:

Excess

Excess is an amount you pay towards the cost of your treatment. When you reach the excess limit, you won't have to contribute further, for example:

So as you can see, once you've covered your excess, your insurer steps in and will start making payments.

Most insurers will charge you one excess per policy term no matter how many times you claim. Others, however, may charge an excess per claim so it's important to understand how excess is charged, as this can add up if you make several claims each year.

You can usually choose the amount of excess you pay. Broadly, the higher the excess amount, the lower your overall premium.

Some health insurance providers offer £0 excess so you won't have to contribute to the cost of treatment, but choosing this will usually result in a significantly higher premium.

Don't forget that if your policy has an excess, it should be a figure you can afford as you must pay it in order to have treatment.

Shared responsibility

Also known as co-payment or 'co-pay' this is where you share the cost of every treatment with your insurer up to an agreed amount. For example, provider WPA offers a shared responsibility model where they cover 75% of the treatment cost with the remaining 25% paid by the policyholder.

No claims discount

Unlike with other types of insurance, such as car or home, where you start with no no claim discount and work your way up as long as you don't claim, with health insurance, new policies come with a no claims discount of around 70%. While on the face of it, this looks good, as it means your premiums are being heavily discounted, there's more discount to lose than there is to gain. Most insurers will limit the number of levels you can fall on their NCD scale to 3 per policy year, but you can still slip down the scale pretty quickly if you have claims, and your premiums will rise accordingly.

Pooled risk and community-rated

Pooled risk and community rated refer to the way premiums are pooled in order to spread risk; this can help bring down premiums for all policyholders in the pool.

If you choose a policy that offers premiums based on pooled risk, what you pay will be affected by the expected number of claims made by the pool. So even if you were considered at higher risk of making a claim, being in a pool with people unlikely to claim dilutes the overall risk, subsequently you could pay less. In contrast, a no claims discount is based on your individual actions and whether or not you've made a claim.

A knowledgeable and competent agent dealt with my health insurance needs. She saved me £600 per month by finding a quote more suited to my needs and budget than my previous company.

Rated Excellent 5/5 on Google Review

Taking all these areas into consideration, it's no wonder that private health insurance feels confusing. But knowing what these different terms mean and understanding what affects your premium and how you can manage it can help you find a policy that works for you.

Also, remember that there's no such thing as one size fits all with insurance; much of it will depend on your circumstances, so consider:

What features are important to you

Most health insurance plans come with a core package that includes inpatient care (this covers overnight stays in hospital). Policies often include cancer care and some outpatient care as standard too.

You can add extra features for a fee, for example, you could increase the level of outpatient treatment that's included or opt for mental health treatment.

If you want your policy to be clear about what's covered, one with full medical underwriting might be worth considering, although they can take longer to arrange, and you may need a medical. Moratorium policies are quicker and cheaper to take out, but the claims process can be much longer.

What you can do without

Unrestricted consultant and hospital lists might give you the greatest choice when it comes to who treats you and where, but is it something you genuinely need?

Limiting yourself to a guided consultant list or regional hospital network is a practical choice, as most of us would prefer to be treated close to home. Another plus is that guided options can be cost-effective and help keep premiums down.

Your budget

Health insurance will typically become more expensive as you age. This is simply because we become more vulnerable to illness and particular conditions which increases the risk of a claim.

Choosing options like pooled risk instead of a no claims discount could help keep costs manageable as premiums are based on group claims rather than your own. Similarly, opting for a high excess or shared responsibility can also help keep premiums down.

Nevertheless, when you're comparing payment options and structures, be aware of all costs involved. For example, if you're choosing an excess, check to see how this is applied – per policy term or per claim. All this information should be set out within your policy documents.

Using a regulated broker

As it stands, private health insurers set their own terms and can use their own terminology, and that's unlikely to change or be standardised anytime soon. However, having a good idea of how your policy can be structured and understanding the various payment options should help you navigate the pros and cons of each.

If you want more tailored advice about finding the right policy, you can also speak to a regulated broker. They'll be able to search for suitable options according to your needs and budget.

Not only that, a health insurance broker will be able to offer advice as your health needs change, ensuring you have a policy that gives you peace of mind no matter what stage of life you're at.

What our readers say

We're rated Excellent on Google from 160+ reviews. Reviews relate to the service provided by both myTribe and our broker partners.

"The information was very helpful and informative. They put me in touch with an extremely helpful broker. I am now moving to a different provider, on a better policy, at a much reduced premium."

"Absolutely straightforward experience. The lesson? NEVER accept a renewal quote without shopping around!"

"Saved time and gave me a lot of insight. I could not have done that on my own."

Disclaimer: This is general information, not personal advice. Speak to a qualified broker before making a decision. Our broker partners compare policies from a panel of leading UK health insurers, but not all insurers may be available.